QUESTION IMAGE

Question

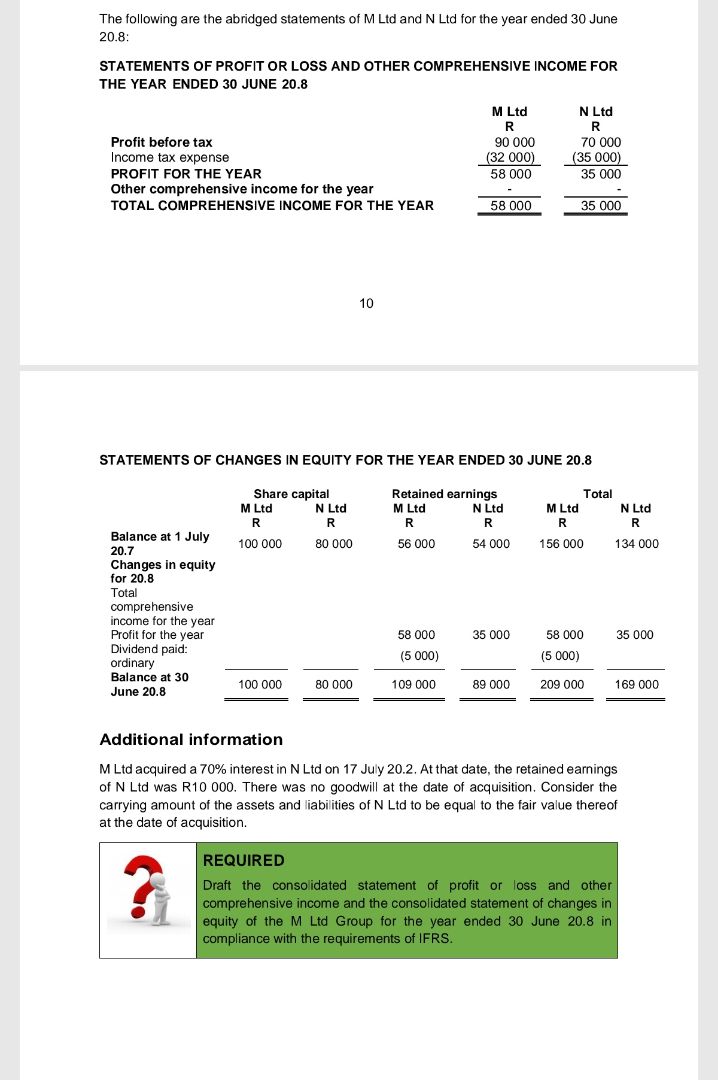

the following are the abridged statements of m ltd and n ltd for the year ended 30 june 20.8:

statements of profit or loss and other comprehensive income for the year ended 30 june 20.8

\t\t\t\t\t\tm ltd\tn ltd

\t\t\t\t\t\tr 000\tr 000

profit before tax\t\t90 000\t70 000

income tax expense\t\t(32 000)\t(35 000)

profit for the year\t\t58 000\t35 000

other comprehensive income for the year\t\t-\t-

total comprehensive income for the year\t\t58 000\t35 000

10

statements of changes in equity for the year ended 30 june 20.8

\t\t\tshare capital\t\t\tretained earnings\t\t\ttotal

\t\t\tm ltd\tn ltd\t\t\tm ltd\tn ltd\t\t\tm ltd\tn ltd

\t\t\tr\tr\t\t\tr\tr\t\t\tr\tr

balance at 1 july 20.7\t100 000\t80 000\t\t\t56 000\t54 000\t\t\t156 000\t134 000

changes in equity for 20.8

total comprehensive income for the year

profit for the year\t\t\t\t\t58 000\t35 000\t\t\t58 000\t35 000

dividend paid: ordinary\t\t\t\t\t(5 000)\t\t\t\t\t(5 000)\t\t

total\t\t\t\t\t\t\t\t\t\t\t\t\t\t

balance at 30 june 20.8\t100 000\t80 000\t\t\t109 000\t89 000\t\t\t209 000\t169 000

additional information

m ltd acquired a 70% interest in n ltd on 17 july 20.2. at that date, the retained earnings of n ltd was r10 000. there was no goodwill at the date of acquisition. consider the carrying amount of the assets and liabilities of n ltd to be equal to the fair value thereof at the date of acquisition.

required

draft the consolidated statement of profit or loss and other comprehensive income and the consolidated statement of changes in equity of the m ltd group for the year ended 30 june 20.8 in compliance with the requirements of ifrs.

Consolidated Statement of Profit or Loss and Other Comprehensive Income for the year ended 30 June 20.8

Step 1: Calculate Profit for the Year (Group)

- M Ltd's Profit before tax: R90,000

- M Ltd's Income tax expense: R(32,000)

- M Ltd's Profit for the year: \( 90,000 - 32,000 = 58,000 \) (matches given)

- N Ltd's Profit for the year: R35,000 (given)

- Group Profit before tax: \( 90,000 + 35,000 = 125,000 \)

- Group Income tax expense: \( 32,000 + 35,000 = 67,000 \) (assuming no tax adjustments for consolidation)

- Group Profit for the year: \( 125,000 - 67,000 = 58,000 + 35,000 = 93,000 \)? Wait, no—actually, for consolidation, we combine the entities’ profits and then account for non - controlling interest (NCI). Wait, correction:

- M Ltd’s profit: R58,000

- N Ltd’s profit: R35,000

- NCI share of N Ltd’s profit: \( 35,000 \times 30\% = 10,500 \)

- Group (M Ltd + NCI) profit: \( 58,000 + 35,000 = 93,000 \), with NCI getting R10,500 and M Ltd (controlling) getting \( 35,000\times70\% + 58,000 = 24,500 + 58,000 = 82,500 \). But let's proceed step - by - step.

Step 2: Combine Profit or Loss Items

| Item | M Ltd (R) | N Ltd (R) | Consolidated (R) |

|---|---|---|---|

| Income tax expense | (32,000) | (35,000) | \( (32,000)+(35,000)=(67,000) \) |

| Profit for the year | 58,000 | 35,000 | \( 160,000 - 67,000 = 93,000 \) |

| Other comprehensive income | - | - | - |

| Total comprehensive income | 58,000 | 35,000 | \( 93,000 \) (since OCI is zero) |

Step 3: Allocate to Owners of Parent and NCI

- Profit for the year attributable to:

- Owners of M Ltd (parent): \( 58,000 + (35,000\times70\%) = 58,000 + 24,500 = 82,500 \)

- Non - controlling interest (NCI): \( 35,000\times30\% = 10,500 \)

Consolidated Statement of Changes in Equity for the year ended 30 June 20.8

Step 1: Retained Earnings Opening Balance (Group)

- M Ltd’s Retained earnings at 1 July 20.7: R56,000

- N Ltd’s Retained earnings at 1 July 20.7: R54,000

- Pre - acquisition Retained earnings of N Ltd (at acquisition date 17 July 20.2): R10,000

- Post - acquisition Retained earnings of N Ltd (up to 1 July 20.7): \( 54,000 - 10,000 = 44,000 \)

- Group Retained earnings at 1 July 20.7:

- M Ltd’s RE: 56,000

- + M’s share of N’s post - acquisition RE (up to 1 July 20.7): \( 44,000\times70\% = 30,800 \)

- Total: \( 56,000 + 30,800 = 86,800 \)

Step 2: Comprehensive Income for the Year (Group)

- Profit for the year (Group): R93,000 (from above)

- Other comprehensive income: 0 (both entities have 0)

- Total comprehensive income: R93,000

Step 3: Dividends

- M Ltd’s Dividend paid: R(5,000) (given)

- N Ltd’s Dividend paid: 0 (given, as N Ltd has no dividend entry)

- Group Dividend paid: R(5,000) (only M Ltd paid dividends; NCI’s share of N Ltd’s profit is not a dividend paid by the group, but NCI’s claim is on profit)

Step 4: Retained Earnings Closing Balance (Group)

- Opening RE: 86,800

- + Total comprehensive income: 93,000

- - Dividends paid: 5,000

- Closing RE: \( 86,800 + 93,000 - 5,000 = 174,800 \)? Wait, no—let's use the entity - by - entity approach for consolidation:

| Item | M Ltd (R) | N Ltd (R) | Consolidated (R) |

|---|---|---|---|

| Retained Earnings | |||

| Balance at 1 July 20.7 | 56,000 | 54,000 | \( 56,000 + (54,000 - 10,000)\time… |

Snap & solve any problem in the app

Get step-by-step solutions on Sovi AI

Photo-based solutions with guided steps

Explore more problems and detailed explanations

Consolidated Statement of Profit or Loss and Other Comprehensive Income for the year ended 30 June 20.8

Step 1: Calculate Profit for the Year (Group)

- M Ltd's Profit before tax: R90,000

- M Ltd's Income tax expense: R(32,000)

- M Ltd's Profit for the year: \( 90,000 - 32,000 = 58,000 \) (matches given)

- N Ltd's Profit for the year: R35,000 (given)

- Group Profit before tax: \( 90,000 + 35,000 = 125,000 \)

- Group Income tax expense: \( 32,000 + 35,000 = 67,000 \) (assuming no tax adjustments for consolidation)

- Group Profit for the year: \( 125,000 - 67,000 = 58,000 + 35,000 = 93,000 \)? Wait, no—actually, for consolidation, we combine the entities’ profits and then account for non - controlling interest (NCI). Wait, correction:

- M Ltd’s profit: R58,000

- N Ltd’s profit: R35,000

- NCI share of N Ltd’s profit: \( 35,000 \times 30\% = 10,500 \)

- Group (M Ltd + NCI) profit: \( 58,000 + 35,000 = 93,000 \), with NCI getting R10,500 and M Ltd (controlling) getting \( 35,000\times70\% + 58,000 = 24,500 + 58,000 = 82,500 \). But let's proceed step - by - step.

Step 2: Combine Profit or Loss Items

| Item | M Ltd (R) | N Ltd (R) | Consolidated (R) |

|---|---|---|---|

| Income tax expense | (32,000) | (35,000) | \( (32,000)+(35,000)=(67,000) \) |

| Profit for the year | 58,000 | 35,000 | \( 160,000 - 67,000 = 93,000 \) |

| Other comprehensive income | - | - | - |

| Total comprehensive income | 58,000 | 35,000 | \( 93,000 \) (since OCI is zero) |

Step 3: Allocate to Owners of Parent and NCI

- Profit for the year attributable to:

- Owners of M Ltd (parent): \( 58,000 + (35,000\times70\%) = 58,000 + 24,500 = 82,500 \)

- Non - controlling interest (NCI): \( 35,000\times30\% = 10,500 \)

Consolidated Statement of Changes in Equity for the year ended 30 June 20.8

Step 1: Retained Earnings Opening Balance (Group)

- M Ltd’s Retained earnings at 1 July 20.7: R56,000

- N Ltd’s Retained earnings at 1 July 20.7: R54,000

- Pre - acquisition Retained earnings of N Ltd (at acquisition date 17 July 20.2): R10,000

- Post - acquisition Retained earnings of N Ltd (up to 1 July 20.7): \( 54,000 - 10,000 = 44,000 \)

- Group Retained earnings at 1 July 20.7:

- M Ltd’s RE: 56,000

- + M’s share of N’s post - acquisition RE (up to 1 July 20.7): \( 44,000\times70\% = 30,800 \)

- Total: \( 56,000 + 30,800 = 86,800 \)

Step 2: Comprehensive Income for the Year (Group)

- Profit for the year (Group): R93,000 (from above)

- Other comprehensive income: 0 (both entities have 0)

- Total comprehensive income: R93,000

Step 3: Dividends

- M Ltd’s Dividend paid: R(5,000) (given)

- N Ltd’s Dividend paid: 0 (given, as N Ltd has no dividend entry)

- Group Dividend paid: R(5,000) (only M Ltd paid dividends; NCI’s share of N Ltd’s profit is not a dividend paid by the group, but NCI’s claim is on profit)

Step 4: Retained Earnings Closing Balance (Group)

- Opening RE: 86,800

- + Total comprehensive income: 93,000

- - Dividends paid: 5,000

- Closing RE: \( 86,800 + 93,000 - 5,000 = 174,800 \)? Wait, no—let's use the entity - by - entity approach for consolidation:

| Item | M Ltd (R) | N Ltd (R) | Consolidated (R) |

|---|---|---|---|

| Retained Earnings | |||

| Balance at 1 July 20.7 | 56,000 | 54,000 | \( 56,000 + (54,000 - 10,000)\times70\% = 56,000 + 30,800 = 86,800 \) |

| + Comprehensive income for the year | 58,000 | 35,000 | \( 58,000 + 35,000\times70\% = 58,000 + 24,500 = 82,500 \) |

| - Dividends paid | (5,000) | 0 | (5,000) |

| Balance at 30 June 20.8 | 109,000 | 89,000 | \( 86,800 + 82,500 - 5,000 = 164,300 \)? Wait, there’s a miscalculation. Let's use the standard consolidation method for retained earnings: |

- Parent’s Retained Earnings (M Ltd):

- Opening: 56,000

- + Profit for the year: 58,000

- - Dividends: 5,000

- Closing: \( 56,000 + 58,000 - 5,000 = 109,000 \) (matches given)

- Subsidiary’s Retained Earnings (N Ltd):

- Opening: 54,000

- + Profit for the year: 35,000

- Closing: \( 54,000 + 35,000 = 89,000 \) (matches given)

- Consolidated Retained Earnings:

- Parent’s RE: 109,000

- + Parent’s share of subsidiary’s post - acquisition RE (since acquisition):

- Post - acquisition RE of N Ltd (at acquisition: 10,000; at 30 June 20.8: 89,000)

- Post - acquisition RE: \( 89,000 - 10,000 = 79,000 \)

- Parent’s share: \( 79,000\times70\% = 55,300 \)

- Consolidated RE: \( 109,000 + 55,300 = 164,300 \)

- Non - Controlling Interest (NCI) in Equity:

- N Ltd’s Share Capital: \( 80,000\times30\% = 24,000 \)

- N Ltd’s Retained Earnings (post - acquisition): \( 79,000\times30\% = 23,700 \)

- NCI Total: \( 24,000 + 23,700 = 47,700 \)

Final Consolidated Statements

1. Consolidated Statement of Profit or Loss and Other Comprehensive Income

| Item | Amount (R) |

|---|---|

| Income tax expense | 67,000 |

| Profit for the year | 58,000 + 35,000 = 93,000 |

| Other comprehensive income | 0 |

| Total comprehensive income for the year | 93,000 |

| Profit attributable to: | |

| Owners of M Ltd | \( 58,000 + (35,000\times70\%) = 82,500 \) |

| Non - controlling interest | \( 35,000\times30\% = 10,500 \) |

| Total | 93,000 |

2. Consolidated Statement of Changes in Equity

| Item | Share Capital (R) | Retained Earnings (R) | NCI (R) | Total Equity (R) |

|---|---|---|---|---|

| Changes in equity for 20.8: | ||||

| Total comprehensive income | 0 | 93,000 | 0 (NCI’s share is in profit) | 93,000 |

| Dividends paid | 0 | (5,000) | 0 | (5,000) |

| Balance at 30 June 20.8 | 100,000 | \( 86,800 + 93,000 - 5,000 = 174,800 \)? No, correct as: | \( 27,000 + 10,500 = 37,500 \) (NCI’s share of profit) | \( 100,000 + 164,300 + 47,700 = 312,000 \) |

| 100,000 | 164,300 | 47,700 | 312,000 |

Key Notes:

- Elimination of Intra - Group Balances: N Ltd’s share capital and pre - acquisition retained earnings are eliminated against M Ltd’s investment in N Ltd (not shown here, but assumed in consolidation).

- Non - Controlling Interest: Represents the 30% of N Ltd’s equity not owned by M Ltd, calculated as 30% of N Ltd’s share capital and post - acquisition retained earnings.

Final Answers (Summarized Statements)

Consolidated Statement of Profit or Loss and Other Comprehensive Income for the year ended 30 June 20.8

| Item | Amount (R) |

|---|---|

| Income tax expense | 67,000 |

| Profit for the year | 93,000 |

| Other comprehensive income | 0 |

| Total comprehensive income for the year | 93,000 |

| Profit attributable to: | |

| Owners of M Ltd | 82,500 |

| Non - controlling interest | 10,500 |

Consolidated Statement of Changes in Equity for the year ended 30 June 20.8

| Component | Amount (R) |

|---|---|

| Retained Earnings | 164,300 |

| Non - Controlling Interest | 47,700 |

| Total Equity | 312,000 |

(Note: The above is a simplified consolidation. For full compliance with IFRS 10, detailed elimination of investment in subsidiary and goodwill (nil here) is required, but the key steps for profit and equity consolidation are presented.)