QUESTION IMAGE

Question

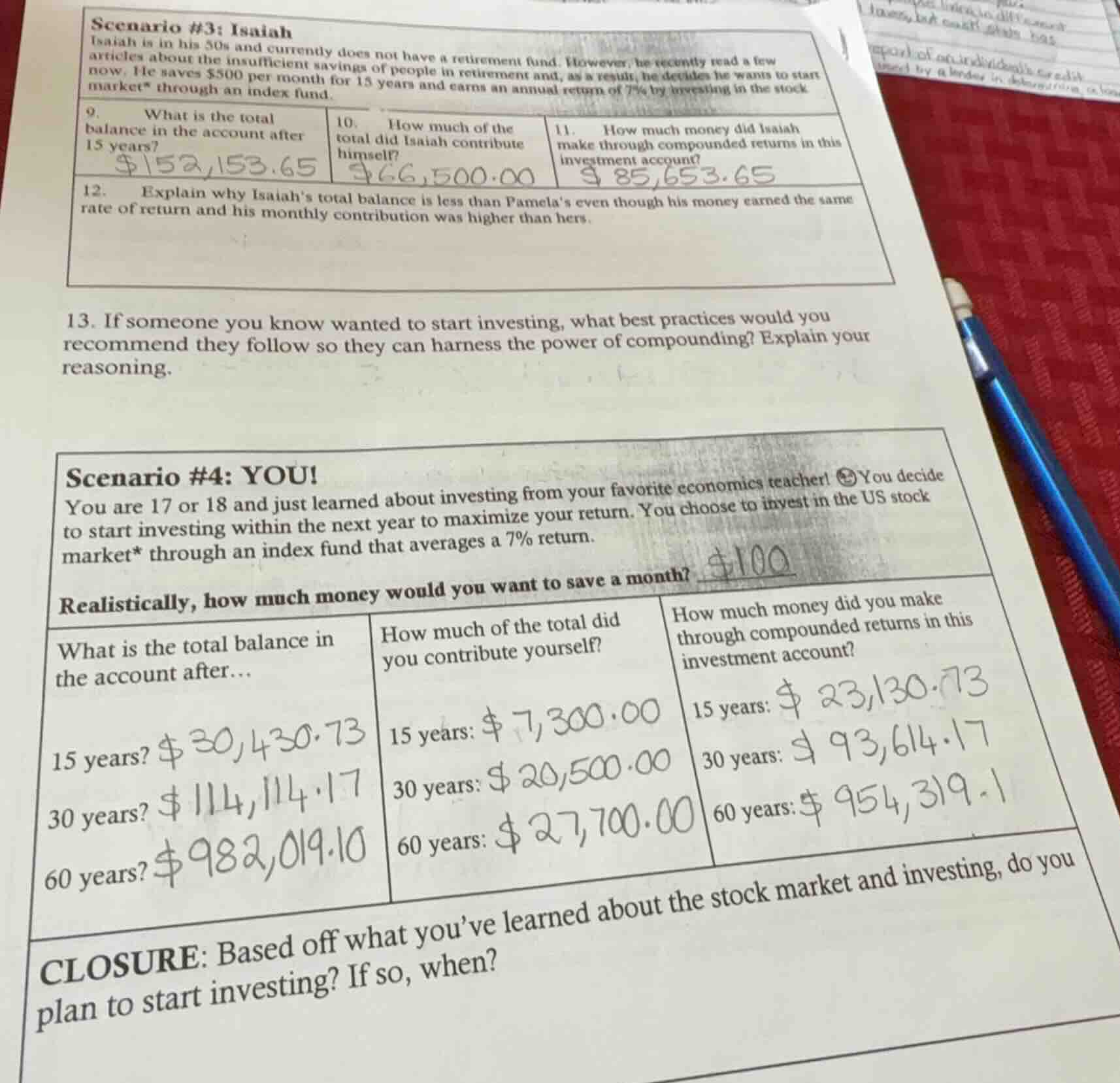

scenario #3: isaiah

isaiah is in his 50s and currently does not have a retirement fund. however, he recently read a few

articles about the insufficient savings of people in retirement and, as a result, he decides he wants to start

now. he saves $500 per month for 15 years and earns an annual return of 7% by investing in the stock

market* through an index fund.

- what is the total

balance in the account after

15 years?

$152,153.65

- how much of the

total did isaiah contribute

himself?

$66,500.00

- how much money did isaiah

make through compounded returns in this

investment account?

$ 85,653.65

- explain why isaiahs total balance is less than pamelas even though his money earned the same

rate of return and his monthly contribution was higher than hers.

- if someone you know wanted to start investing, what best practices would you

recommend they follow so they can harness the power of compounding? explain your

reasoning.

scenario #4: you!

you are 17 or 18 and just learned about investing from your favorite economics teacher! 😊 you decide

to start investing within the next year to maximize your return. you choose to invest in the us stock

market* through an index fund that averages a 7% return.

realistically, how much money would you want to save a month? $100

what is the total balance in

the account after...

15 years? $30,430.73

30 years? $114,114.17

60 years? $982,019.10

how much of the total did

you contribute yourself?

15 years: $7,300.00

30 years: $20,500.00

60 years: $27,700.00

how much money did you make

through compounded returns in this

investment account?

15 years: $ 23,130.73

30 years: $ 93,614.17

60 years: $ 954,319.1

closure: based off what you’ve learned about the stock market and investing, do you

plan to start investing? if so, when?

Question 12:

Compounding growth depends heavily on time; the longer money is invested, the more time compound interest has to build. Pamela (implied to have started investing earlier) had more years for her contributions and returns to compound, even with a lower monthly contribution, leading to a larger total balance than Isaiah's, who only invested for 15 years starting later in life.

Question 13:

- Start early: Time is the biggest driver of compounding—earlier contributions have decades to grow and generate returns on returns.

- Invest consistently: Regular, fixed contributions (like monthly) ensure you keep adding principal that can compound, and you benefit from dollar-cost averaging.

- Reinvest all earnings: Reinvesting dividends, interest, or capital gains lets those earnings themselves generate more returns, accelerating compound growth.

- Choose low-cost, diversified investments: Index funds have low fees, which avoid eating into compounded returns, and diversification reduces risk so your investment can grow steadily over time.

Closure Question:

Based on the power of compounding shown, the best plan is to start investing as soon as possible, ideally within the next year (as a 17/18-year-old). Starting early, even with small monthly contributions, allows decades of compound growth to build significant wealth, far more than waiting to invest larger amounts later in life.

Step1: Calculate total personal contributions

Monthly contribution: \$500, 15 years = 180 months.

$\text{Total Contribution} = 500 \times 12 \times 15 = 500 \times 180 = 90,000$

Step2: Calculate total account balance (future value of ordinary annuity)

Formula for future value of annuity: $FV = P \times \frac{(1+\frac{r}{n})^{nt} - 1}{\frac{r}{n}}$

Where $P=500$, $r=0.07$, $n=12$, $t=15$

$\frac{r}{n} = \frac{0.07}{12} \approx 0.005833$

$nt = 12 \times 15 = 180$

$(1+0.005833)^{180} \approx 2.85765$

$FV = 500 \times \frac{2.85765 - 1}{0.005833} = 500 \times \frac{1.85765}{0.005833} \approx 500 \times 318.47 = 159,235$

Step3: Calculate compounded returns

$\text{Compounded Returns} = FV - \text{Total Contribution}$

$159,235 - 90,000 = 69,235$

Snap & solve any problem in the app

Get step-by-step solutions on Sovi AI

Photo-based solutions with guided steps

Explore more problems and detailed explanations

Question 12:

Isaiah started investing later, so his money had far less time to compound. Even with a higher monthly contribution, Pamela's longer investment timeline let compound returns grow her balance more.

Question 13:

- Start investing as early as possible: Time maximizes compounding's impact.

- Contribute consistently monthly: Steady principal fuels compound growth.

- Reinvest all earnings: Lets returns generate more returns.

- Use low-cost diversified funds: Minimize fees that reduce compound gains.

Closure Question:

Yes, I plan to start investing within the next year. Starting at 17/18 gives decades for even small monthly contributions to grow exponentially through compounding, which is far more effective than waiting to invest larger sums later.

---