QUESTION IMAGE

Question

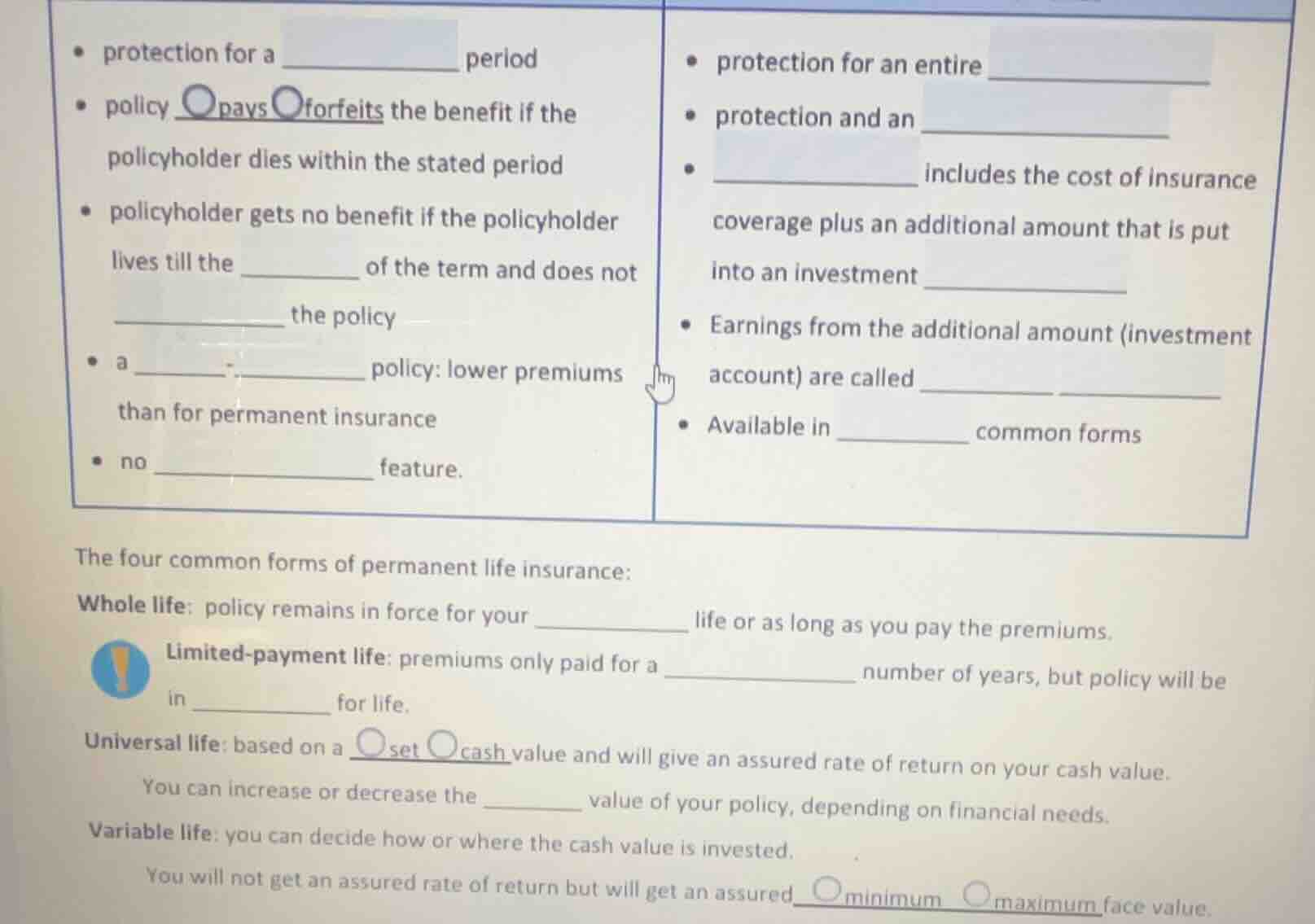

- protection for a _________ period

- policy (\bigcirc) pays (\bigcirc) forfeits the benefit if the

policyholder dies within the stated period

- policyholder gets no benefit if the policyholder

lives till the ______ of the term and does not

________ the policy

- a ___: _____ policy: lower premiums

than for permanent insurance

- no __________ feature.

- protection for an entire __________

- protection and an __________

- _________ includes the cost of insurance

coverage plus an additional amount that is put

into an investment __________

- earnings from the additional amount (investment

account) are called ____ _____

- available in ______ common forms

the four common forms of permanent life insurance:

whole life: policy remains in force for your ________ life or as long as you pay the premiums.

limited - payment life: premiums only paid for a __________ number of years, but policy will be

in _______ for life.

universal life: based on a (\bigcirc) set (\bigcirc) cash value and will give an assured rate of return on your cash value.

you can increase or decrease the _____ value of your policy, depending on financial needs.

variable life: you can decide how or where the cash value is invested.

you will not get an assured rate of return but will get an assured (\bigcirc) minimum (\bigcirc) maximum face value.

This appears to be a fill - in - the - blank exercise related to insurance, specifically life insurance policies. Let's analyze each blank:

Left Column (Term Life Insurance - likely)

- "protection for a \_\_\_\_\_\_\_\_ period": The typical term for term life insurance is a "specific" or "stated" period, but more accurately, "limited" (since term life is for a limited time). But a more common fill - in here is "specific" or "fixed". However, the standard term is "term" (so "protection for a term period" but that's a bit redundant. Alternatively, "limited" or "specific".

- "policy \_\_ pays \_\_ forfeits the benefit if the policyholder dies within the stated period": The correct option is "pays" (the policy pays the benefit if the policyholder dies within the term).

- "policyholder gets no benefit if the policyholder lives till the \_\_\_\_\_ of the term and does not \_\_\_\_\_ the policy": The first blank is "end" (till the end of the term), the second blank is "renew" (if they don't renew the policy).

- "a \_\_ - \_\_\_\_ policy: lower premiums than for permanent insurance": This is "term - life" policy.

- "no \_\_\_\_\_\_\_\_ feature": Term life has no "cash - value" feature.

Right Column (Permanent Life Insurance - likely)

- "protection for an entire \_\_\_\_\_\_\_\_": "lifetime" (protection for an entire lifetime).

- "protection and an \_\_\_\_\_\_\_\_": "investment component" (permanent life has both protection and an investment component).

- "\_\_\_\_\_\_\_\_ includes the cost of insurance coverage plus an additional amount that is put into an investment \_\_\_\_\_\_\_\_": The first blank is "Premium" (the premium includes...), the second blank is "account".

- "Earnings from the additional amount (investment account) are called \_\_\_\_\_ \_\_\_\_\_\_": "cash value" (the earnings from the investment part contribute to the cash value, but more accurately, "dividends" or "interest" but in the context of whole life, it can be "cash value growth" or more precisely, "cash value" (the earnings are part of the cash value). Wait, for universal or whole life, the earnings on the investment part (the cash value) are either interest (for universal) or dividends (for whole life). But a more general term here could be "cash value" or "investment earnings". However, the standard term is that the earnings from the investment account in permanent life insurance (like whole life) are used to build the "cash value", and the earnings themselves can be called "dividends" (for participating whole life) or "interest" (for universal life). But a common fill - in here is "cash value" (but the question says "Earnings... are called...", so maybe "policy dividends" or "investment income".

- "Available in \_\_\_\_\_ common forms": "four" (as the text below says "The four common forms...")

Below the Columns (Permanent Life Insurance Forms)

- "Whole life: policy remains in force for your \_\_\_\_\_\_\_\_ life or as long as you pay the premiums": "entire" (your entire life).

- "Limited - payment life: premiums only paid for a \_\_\_\_\_\_\_\_ number of years, but policy will be in \_\_\_\_\_ for life.": The first blank is "limited" (a limited number of years), the second blank is "force" (in force for life).

- "Universal life: based on a \_\_ set \_\_ cash value and will give an assured rate of return on your cash value. You can increase or decrease the \_\_ value of your policy, depending on financial needs.": The first two blanks: the correct option is "cash" (based on a cash value, and the option is "cash" (the circle is on "ca…

The exercise is about differentiating between term life (temporary, no cash value, lower premiums) and permanent life (lifetime coverage, cash value, investment component) insurance policies. The blanks are filled based on the characteristics of these two types of life insurance and their sub - types (whole, limited - payment, universal, variable).

Snap & solve any problem in the app

Get step-by-step solutions on Sovi AI

Photo-based solutions with guided steps

Explore more problems and detailed explanations

s:

- Left Column (Term Life - assumed):

- protection for a limited period

- policy pays the benefit if the policyholder dies within the stated period

- policyholder gets no benefit if the policyholder lives till the end of the term and does not renew the policy

- a term - life policy: lower premiums than for permanent insurance

- no cash - value feature

- Right Column (Permanent Life - assumed):

- protection for an entire lifetime

- protection and an investment component

- Premium includes the cost of insurance coverage plus an additional amount that is put into an investment account

- Earnings from the additional amount (investment account) are called cash value (or dividends/interest)

- Available in four common forms

- Permanent Life Forms:

- Whole life: policy remains in force for your entire life or as long as you pay the premiums

- Limited - payment life: premiums only paid for a limited number of years, but policy will be in force for life

- Universal life: based on a cash value and will give an assured rate of return on your cash value. You can increase or decrease the face value of your policy, depending on financial needs

- Variable life: you can decide how or where the cash value is invested. You will not get an assured rate of return but will get an assured minimum face value