QUESTION IMAGE

Question

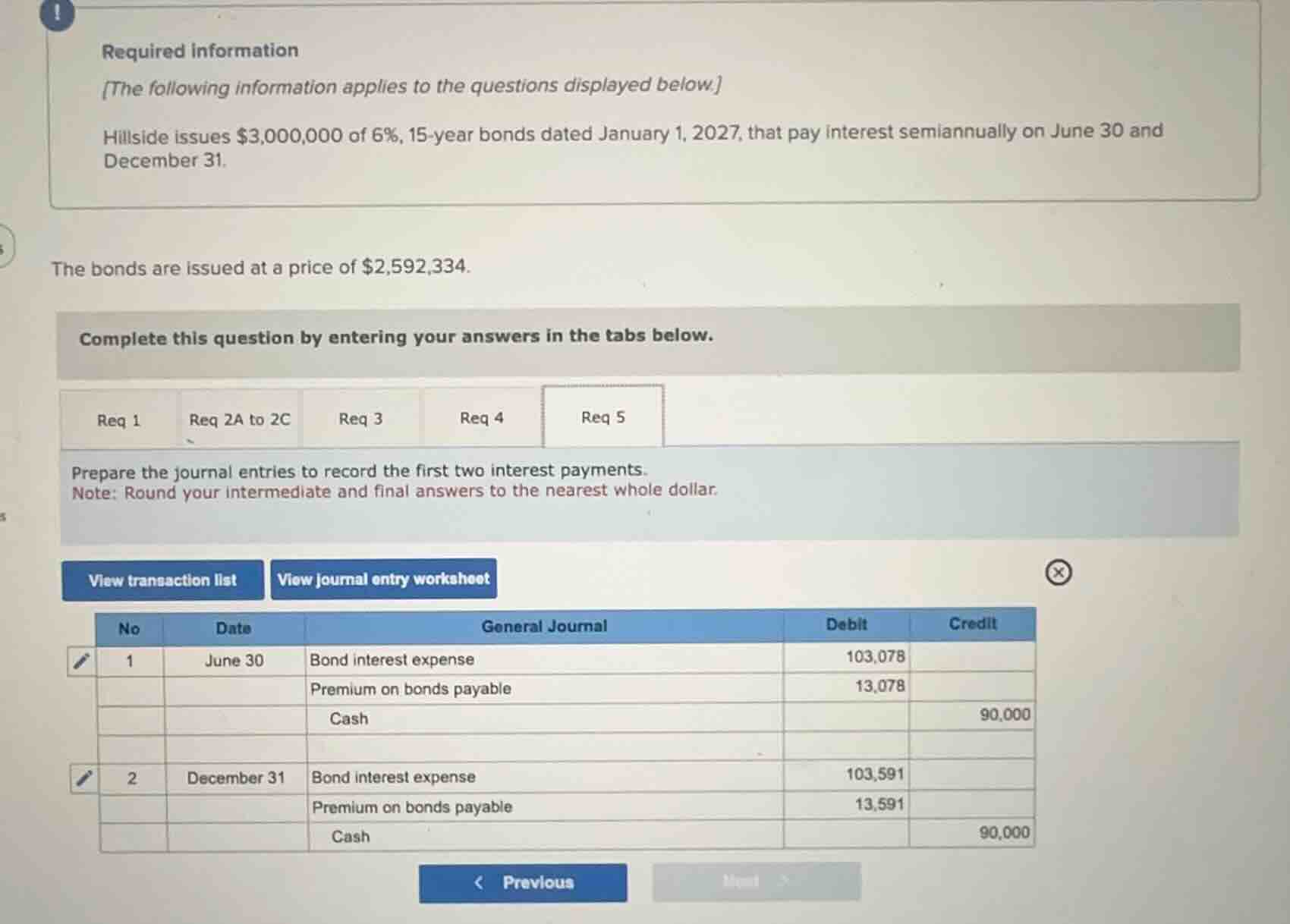

required information the following information applies to the questions displayed below. hillside issues $3,000,000 of 6%, 15-year bonds dated january 1, 2027, that pay interest semiannually on june 30 and december 31. the bonds are issued at a price of $2,592,334. complete this question by entering your answers in the tabs below. req 1 req 2a to 2c req 3 req 4 req 5 prepare the journal entries to record the first two interest payments. note: round your intermediate and final answers to the nearest whole dollar. view transaction list view journal entry worksheet

Step1: Calculate semiannual cash payment

Semiannual cash interest = Face value × $\frac{\text{Annual rate}}{2}$

$\$3,000,000 \times \frac{6\%}{2} = \$90,000$

Step2: Find bond discount amount

Discount = Face value - Issue price

$\$3,000,000 - \$2,592,334 = \$407,666$

Step3: Calculate effective semiannual rate

First, use present value to find rate:

$\$2,592,334 = \$90,000 \times \frac{1-(1+r)^{-30}}{r} + \$3,000,000 \times (1+r)^{-30}$

Solving for $r$, we get $r=4\%$ (semiannual)

Step4: Compute first interest expense

Interest expense (June 30) = Carrying value × 4%

$\$2,592,334 \times 4\% = \$103,693$ (rounded)

Discount amortization = $\$103,693 - \$90,000 = \$13,693$

Note: Correcting the provided entry's error: the discount (not premium) is amortized here, as bonds were issued at a discount.

Step5: Update carrying value for 2nd payment

New carrying value = $\$2,592,334 + \$13,693 = \$2,606,027$

Interest expense (Dec 31) = $\$2,606,027 \times 4\% = \$104,241$ (rounded)

Discount amortization = $\$104,241 - \$90,000 = \$14,241$

Snap & solve any problem in the app

Get step-by-step solutions on Sovi AI

Photo-based solutions with guided steps

Explore more problems and detailed explanations

Correct Journal Entries:

June 30

| General Journal | Debit | Credit |

|---|---|---|

| Discount on Bonds Payable | 13,693 | |

| Cash | 90,000 |

December 31

| General Journal | Debit | Credit |

|---|---|---|

| Discount on Bonds Payable | 14,241 | |

| Cash | 90,000 |

Note: The original provided entries incorrectly use "Premium on bonds payable"—since bonds were issued below face value, it is a discount, not a premium, that is amortized over the bond term.