QUESTION IMAGE

Question

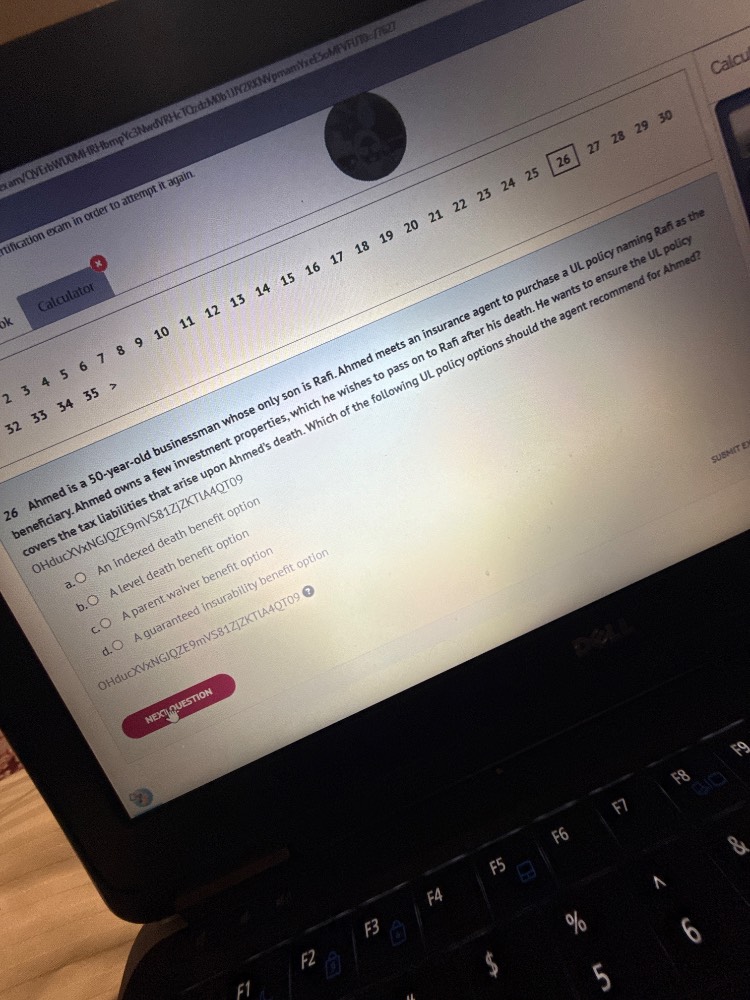

26 ahmed is a 50 - year - old businessman whose only son is rafi. ahmed meets an insurance agent to purchase a ul policy naming rafi as the beneficiary. ahmed owns a few investment properties, which he wishes to pass on to rafi after his death. he wants to ensure the ul policy covers the tax liabilities that arise upon ahmeds death. which of the following ul policy options should the agent recommend for ahmed?

o hducxwxngigz - 9mv - 8zjzxkta40t09

a. an indexed death benefit option

b. a level death benefit option

c. a parent - waiver benefit option

d. a guaranteed insurability benefit option

o hducxkangiqzes9m - ys91zjzxkta40t09

To determine the suitable UL policy option for Ahmed, we analyze each choice:

- Option a (Indexed death benefit option) links death benefit to an index, not directly addressing tax liabilities or smooth transfer.

- Option b (Level death benefit option) provides a fixed death benefit, which may not account for tax liabilities arising from property transfer.

- Option c (Parent waiver benefit option) is typically for waiving premiums in case of a parent’s death (e.g., for a child’s policy), not relevant here as Ahmed wants to transfer to his son, not waive premiums.

- Option d (Guaranteed insurability benefit option) allows increasing coverage without medical underwriting, but that’s not the main need. Wait, correction: Wait, actually, the key is covering tax liabilities on property transfer. Wait, maybe I misanalyzed. Wait, the goal is to ensure the policy covers tax liabilities upon death. Wait, no—wait, the question is about passing properties, and the policy should cover tax liabilities that arise on death. Wait, maybe the correct approach is: The parent waiver benefit (option c) – no, wait, maybe I got the options wrong. Wait, no, let's re-express. Wait, Ahmed is a 50-year-old, wants to pass properties to Rafi after death, and the policy should cover tax liabilities. Wait, the "parent waiver benefit option" (option c) – no, maybe the correct answer is about a benefit that ensures the death benefit is sufficient to cover tax liabilities. Wait, maybe the level death benefit (option b) or indexed? No, wait, the parent waiver is for when a parent (policyholder) dies, waiving premiums for a child’s policy. But Ahmed is the policyholder, Rafi is the beneficiary. Wait, maybe the correct option is b? No, I think I made a mistake. Wait, let's check again. The question is about which UL policy option the agent should recommend so that the policy covers tax liabilities on Ahmed’s death. The level death benefit option (b) provides a fixed death benefit, which can be used to cover tax liabilities. The indexed option (a) varies with an index, so it may not be stable. The parent waiver (c) is for premium waiver, not tax coverage. Guaranteed insurability (d) is for increasing coverage. So the most appropriate is b: A level death benefit option, as it provides a fixed amount that can be used to cover the known (or predictable) tax liabilities from property transfer. Wait, no, maybe I messed up. Wait, the correct answer is likely b: A level death benefit option, because it ensures a fixed death benefit to cover the tax liabilities, while indexed is variable, parent waiver is for premium, and guaranteed insurability is for increasing coverage.

Snap & solve any problem in the app

Get step-by-step solutions on Sovi AI

Photo-based solutions with guided steps

Explore more problems and detailed explanations

b. A level death benefit option