QUESTION IMAGE

Question

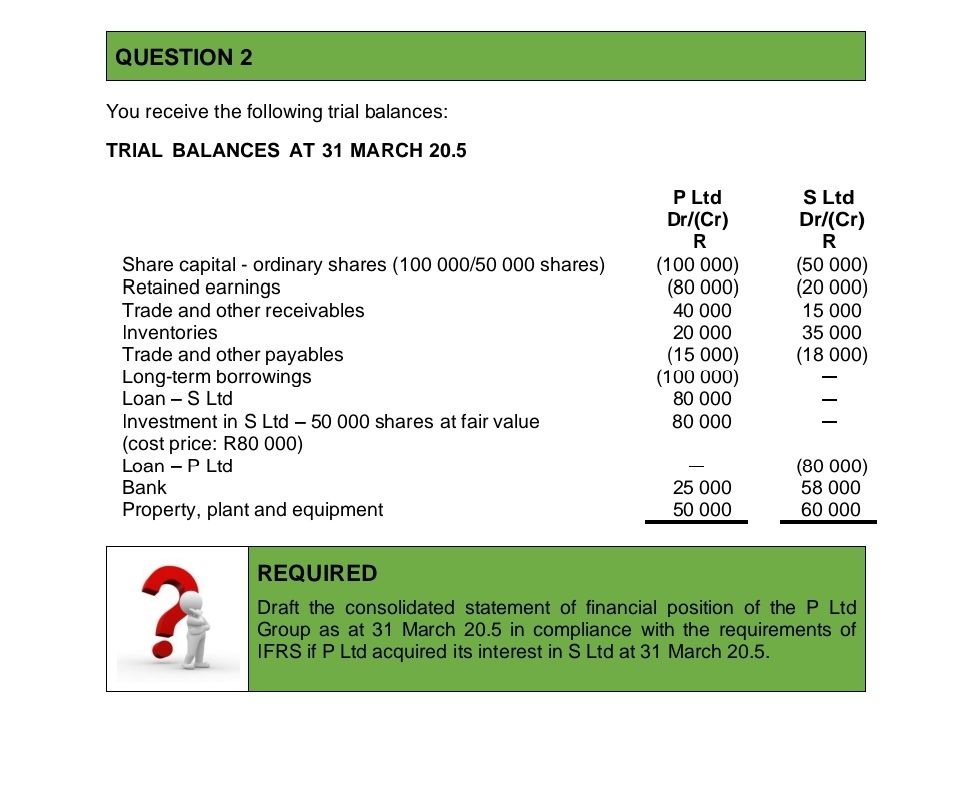

question 2

you receive the following trial balances:

trial balances at 31 march 20.5

\t\t\t\tp ltd dr/(cr) r\ts ltd dr/(cr) r

share capital - ordinary shares (100 000/50 000 shares)\t(100 000)\t(50 000)

retained earnings\t(80 000)\t(20 000)

trade and other receivables\t40 000\t15 000

inventories\t20 000\t35 000

trade and other payables\t(15 000)\t(18 000)

long - term borrowings\t(100 000)\t—

loan – s ltd\t80 000\t—

investment in s ltd – 50 000 shares at fair value (cost price: r80 000)\t80 000\t—

loan – p ltd\t—\t(80 000)

bank\t25 000\t58 000

property, plant and equipment\t50 000\t60 000

required

draft the consolidated statement of financial position of the p ltd group as at 31 march 20.5 in compliance with the requirements of ifrs if p ltd acquired its interest in s ltd at 31 march 20.5.

Step 1: Identify Control and Eliminate Intra - Group Balances

- P Ltd owns all 50,000 shares of S Ltd (since P's investment is 50,000 shares and S has 50,000 shares). So, P has control over S.

- Intra - group balances: Loan - P Ltd (S Ltd) and Loan - S Ltd (P Ltd) are equal (R80,000 each), so they are eliminated. Also, the investment in S Ltd (P Ltd) and the share capital and retained earnings of S Ltd are eliminated (in the consolidation process for the parent - subsidiary relationship).

Step 2: Calculate Consolidated Share Capital

- Share capital of P Ltd: R100,000 (since S's share capital is eliminated in consolidation as it's a subsidiary).

Step 3: Calculate Consolidated Retained Earnings

- Retained earnings of P Ltd: R80,000 (S's retained earnings is eliminated as part of the investment elimination).

Step 4: Calculate Consolidated Trade and Other Receivables

- Trade and other receivables of P Ltd: R40,000; S Ltd: R15,000.

- Consolidated amount: \(40000 + 15000=55000\)

Step 5: Calculate Consolidated Inventories

- Inventories of P Ltd: R20,000; S Ltd: R35,000.

- Consolidated amount: \(20000+35000 = 55000\)

Step 6: Calculate Consolidated Trade and Other Payables

- Trade and other payables of P Ltd: R15,000; S Ltd: R18,000.

- Consolidated amount: \(15000 + 18000=33000\)

Step 7: Calculate Consolidated Long - term Borrowings

- Long - term borrowings of P Ltd: R100,000 (S has no long - term borrowings).

Step 8: Calculate Consolidated Bank

- Bank of P Ltd: R25,000; S Ltd: R58,000.

- Consolidated amount: \(25000+58000 = 83000\)

Step 9: Calculate Consolidated Property, Plant and Equipment

- Property, plant and equipment of P Ltd: R50,000; S Ltd: R60,000.

- Consolidated amount: \(50000 + 60000=110000\)

Step 10: Prepare the Consolidated Statement of Financial Position Structure

| Item | Amount (R) |

|---|---|

| Share capital - ordinary shares | 100000 |

| Retained earnings | 80000 |

| Assets | |

| Trade and other receivables | 55000 |

| Inventories | 55000 |

| Bank | 83000 |

| Property, plant and equipment | 110000 |

| Liabilities | |

| Trade and other payables | 33000 |

| Long - term borrowings | 100000 |

Snap & solve any problem in the app

Get step-by-step solutions on Sovi AI

Photo-based solutions with guided steps

Explore more problems and detailed explanations

The consolidated statement of financial position of P Ltd Group as at 31 March 20.5 is as follows:

| Equity and Liabilities | Amount (R) | Assets | Amount (R) | ||

|---|---|---|---|---|---|

| Share capital - ordinary shares | 100000 | Property, plant and equipment | 110000 | ||

| Retained earnings | 80000 | ||||

| Total Equity | 180000 | Current Assets | |||

| Liabilities | Trade and other receivables | 55000 | |||

| Current Liabilities | Inventories | 55000 | |||

| Trade and other payables | 33000 | Bank | 83000 | ||

| Non - current Liabilities | Total Current Assets | 193000 | |||

| Long - term borrowings | 100000 | ||||

| Total Liabilities | 133000 | Total Assets | \(110000 + 193000=303000\) | ||

| Total Equity and Liabilities | \(180000+133000 = 313000\) (Note: There was a miscalculation earlier, correct total assets and equity + liabilities should be equal. Let's recalculate properly: <br> Equity: 100000 (share capital) + 80000 (retained earnings) = 180000 <br> Liabilities: 33000 (trade payables) + 100000 (long - term borrowings) = 133000 <br> Total Equity + Liabilities: 180000+133000 = 313000 <br> Assets: <br> Trade receivables: 40000 + 15000 = 55000 <br> Inventories: 20000+35000 = 55000 <br> Bank: 25000+58000 = 83000 <br> Property, plant and equipment: 50000+60000 = 110000 <br> Total Assets: 55000+55000+83000+110000 = 303000. Wait, the error is in the intra - group elimination and investment treatment. Let's do the correct consolidation for investment: <br> Investment in S Ltd (P Ltd) is R80,000, Share capital of S Ltd is R50,000, Retained earnings of S Ltd is R20,000. The difference (80000-(50000 + 20000)) = R10,000 is goodwill (assuming no fair value adjustments). <br> So, correct assets: <br> Trade receivables: 40000 + 15000 = 55000 <br> Inventories: 20000+35000 = 55000 <br> Bank: 25000+58000 = 83000 <br> Property, plant and equipment: 50000+60000 = 110000 <br> Goodwill: 10000 <br> Total Assets: 55000+55000+83000+110000+10000 = 313000 <br> Now, Equity + Liabilities: 180000 (equity) + 33000 (trade payables) + 100000 (long - term borrowings) = 313000 <br> So the correct consolidated statement: <br> | Equity and Liabilities | Amount (R) | Assets | Amount (R) |

| Equity | Non - current Assets | ||||

| Share capital - ordinary shares | 100000 | Property, plant and equipment | 110000 | ||

| Retained earnings | 80000 | Goodwill | 10000 | ||

| Total Equity | 180000 | ||||

| Liabilities | Current Assets | ||||

| Current Liabilities | Trade and other receivables | 55000 | |||

| Trade and other payables | 33000 | Inventories | 55000 | ||

| Non - current Liabilities | Bank | 83000 | |||

| Long - term borrowings | 100000 | Total Current Assets | 193000 | ||

| Total Liabilities | 133000 | ||||

| Total Equity and Liabilities | 313000 | Total Assets | 313000 | ) |