QUESTION IMAGE

Question

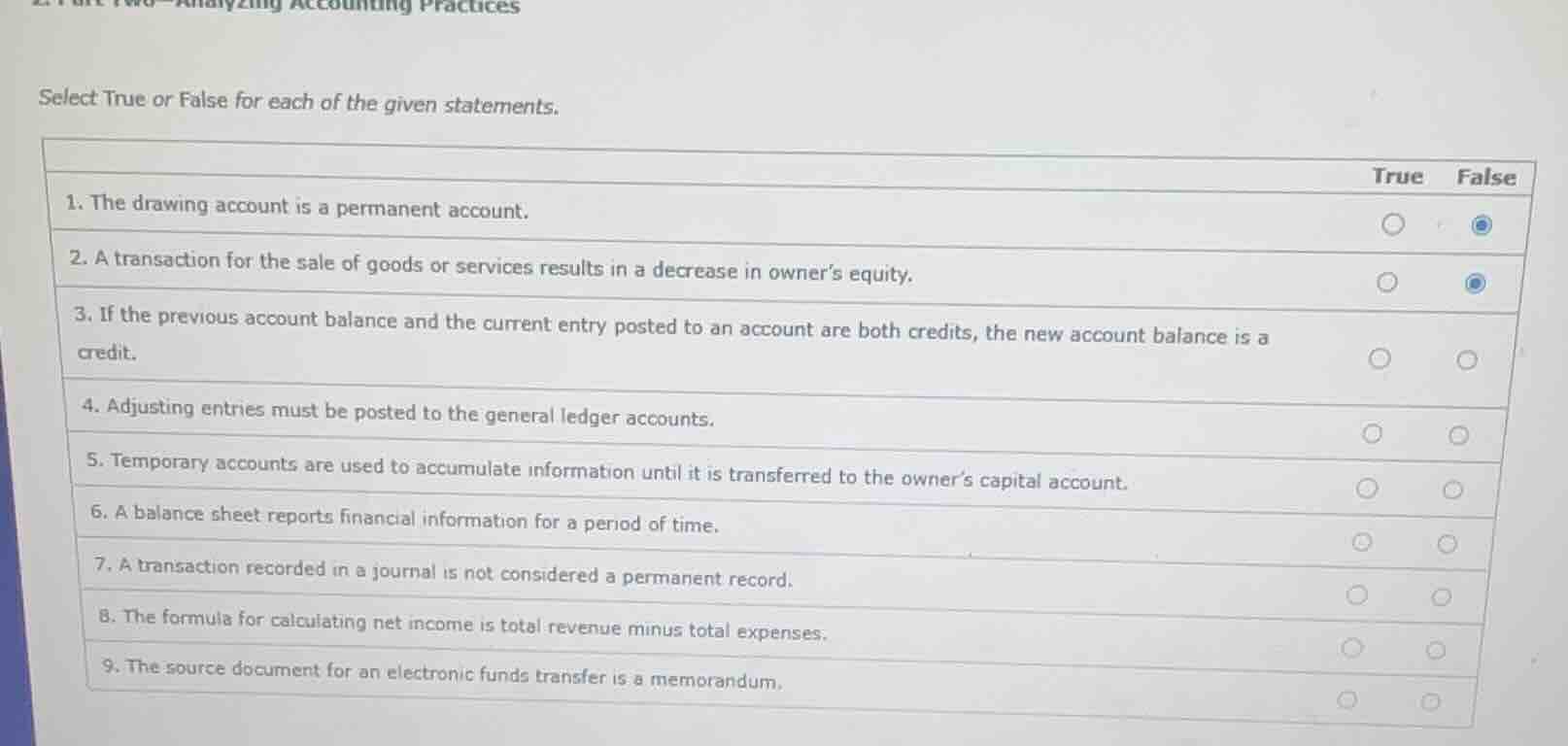

select true or false for each of the given statements.

- the drawing account is a permanent account.

- a transaction for the sale of goods or services results in a decrease in owner’s equity.

- if the previous account balance and the current entry posted to an account are both credits, the new account balance is a credit.

- adjusting entries must be posted to the general ledger accounts.

- temporary accounts are used to accumulate information until it is transferred to the owner’s capital account.

- a balance sheet reports financial information for a period of time.

- a transaction recorded in a journal is not considered a permanent record.

- the formula for calculating net income is total revenue minus total expenses.

- the source document for an electronic funds transfer is a memorandum.

Response

To solve each True/False question, we analyze accounting concepts:

1. The drawing account is a permanent account.

- Drawing accounts are temporary (closed to capital at period - end).

- Answer: False

2. A transaction for the sale of goods or services results in a decrease in owner’s equity.

- Sales increase revenue, which increases net income and thus owner’s equity.

- Answer: False

3. If the previous account balance and the current entry posted to an account are both credits, the new account balance is a credit.

- Credits add to credit balances (e.g., liability accounts: previous credit + new credit = larger credit).

- Answer: True

4. Adjusting entries must be posted to the general ledger accounts.

- Adjusting entries update ledger balances for accuracy (e.g., accruals, deferrals).

- Answer: True

5. Temporary accounts are used to accumulate information until it is transferred to the owner’s capital account.

- Temporary accounts (revenue, expense, drawing) are closed to capital at period - end.

- Answer: True

6. A balance sheet reports financial information for a period of time.

- Balance sheets show financial position at a point in time; income statements show activity over a period.

- Answer: False

7. A transaction recorded in a journal is not considered a permanent record.

- Journals are permanent records of transactions (used to post to ledgers).

- Answer: False

8. The formula for calculating net income is total revenue minus total expenses.

- Net Income = Revenue - Expenses (matches the formula).

- Answer: True

9. The source document for an electronic funds transfer is a memorandum.

- EFTs use a memorandum as a source document (no physical check, so a memo documents the transfer).

- Answer: True

Final Answers (with original question numbers):

- False

- False

- True

- True

- True

- False

- False

- True

- True

Snap & solve any problem in the app

Get step-by-step solutions on Sovi AI

Photo-based solutions with guided steps

Explore more problems and detailed explanations

To solve each True/False question, we analyze accounting concepts:

1. The drawing account is a permanent account.

- Drawing accounts are temporary (closed to capital at period - end).

- Answer: False

2. A transaction for the sale of goods or services results in a decrease in owner’s equity.

- Sales increase revenue, which increases net income and thus owner’s equity.

- Answer: False

3. If the previous account balance and the current entry posted to an account are both credits, the new account balance is a credit.

- Credits add to credit balances (e.g., liability accounts: previous credit + new credit = larger credit).

- Answer: True

4. Adjusting entries must be posted to the general ledger accounts.

- Adjusting entries update ledger balances for accuracy (e.g., accruals, deferrals).

- Answer: True

5. Temporary accounts are used to accumulate information until it is transferred to the owner’s capital account.

- Temporary accounts (revenue, expense, drawing) are closed to capital at period - end.

- Answer: True

6. A balance sheet reports financial information for a period of time.

- Balance sheets show financial position at a point in time; income statements show activity over a period.

- Answer: False

7. A transaction recorded in a journal is not considered a permanent record.

- Journals are permanent records of transactions (used to post to ledgers).

- Answer: False

8. The formula for calculating net income is total revenue minus total expenses.

- Net Income = Revenue - Expenses (matches the formula).

- Answer: True

9. The source document for an electronic funds transfer is a memorandum.

- EFTs use a memorandum as a source document (no physical check, so a memo documents the transfer).

- Answer: True

Final Answers (with original question numbers):

- False

- False

- True

- True

- True

- False

- False

- True

- True