QUESTION IMAGE

Question

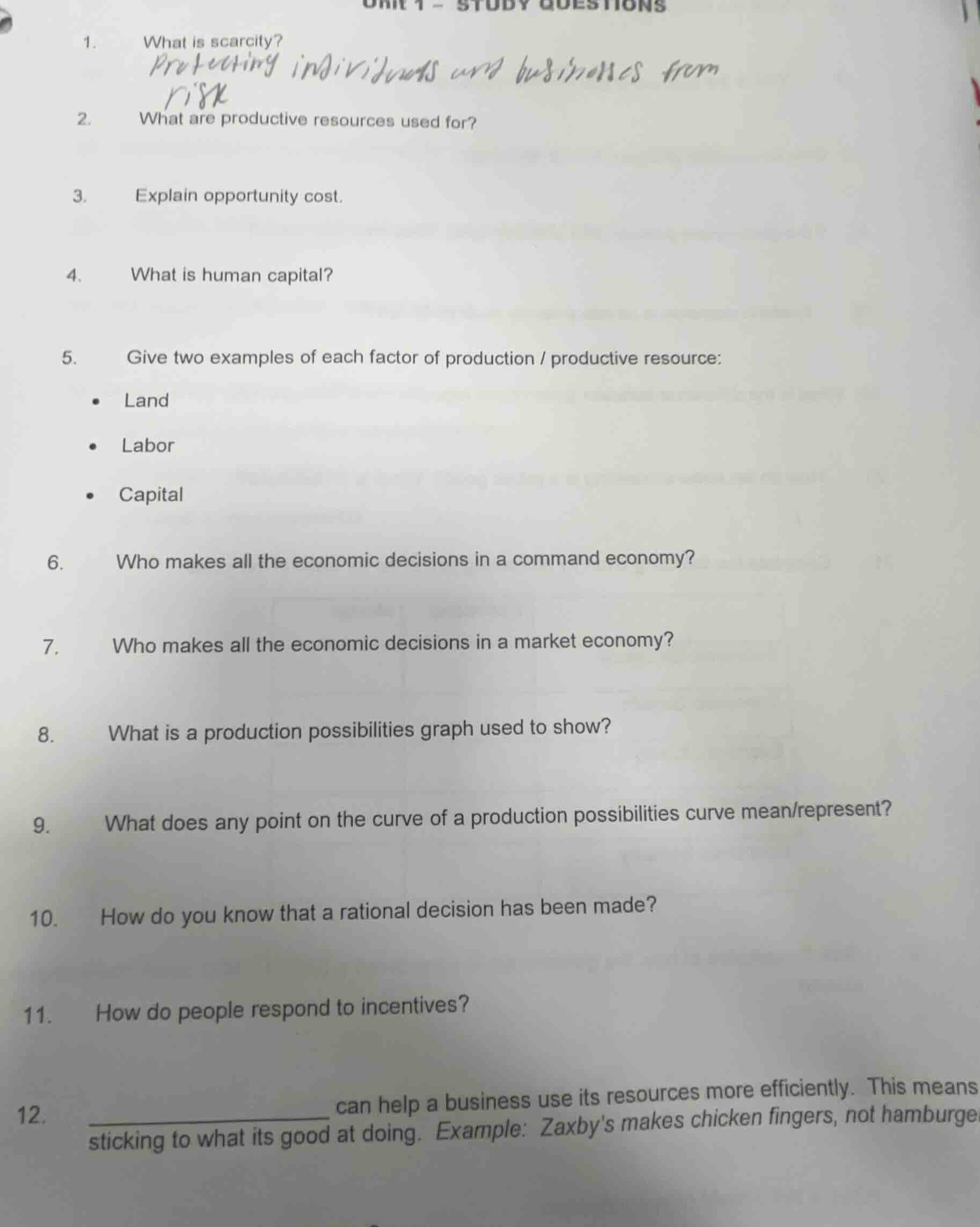

unit 1 - study questions

- what is scarcity?

- what are productive resources used for?

- explain opportunity cost.

- what is human capital?

- give two examples of each factor of production / productive resource:

- land

- labor

- capital

- who makes all the economic decisions in a command economy?

- who makes all the economic decisions in a market economy?

- what is a production possibilities graph used to show?

- what does any point on the curve of a production possibilities curve mean/represent?

- how do you know that a rational decision has been made?

- how do people respond to incentives?

- ______________ can help a business use its resources more efficiently. this means sticking to what its good at doing. example: zaxbys makes chicken fingers, not hamburge

Brief Explanations

- Defined as the fundamental economic condition where unlimited human wants exceed limited available resources.

- Used to produce goods and services to satisfy consumer wants.

- The value of the next-best alternative that is forgone when making a choice.

- The knowledge, skills, education, and experience that workers possess, which boosts their productive capacity.

- Examples tied to core production factors:

- Land: Natural resources for production

- Labor: Human effort in production

- Capital: Man-made production tools

- Centralized government/state authority controls all economic choices.

- Private individuals and businesses (driven by supply/demand) make choices.

- Illustrates maximum output combinations of two goods with fixed resources.

- Represents efficient full utilization of available resources.

- When the marginal benefit of a choice equals or exceeds its marginal cost.

- People act to pursue rewards and avoid penalties, adjusting behavior to gain benefits or reduce losses.

- Focusing on a specific production task to boost efficiency, matching the given example.

Snap & solve any problem in the app

Get step-by-step solutions on Sovi AI

Photo-based solutions with guided steps

Explore more problems and detailed explanations

- Scarcity is the basic economic problem where unlimited human wants and needs exceed the limited resources available to fulfill them.

- Productive resources are used to produce goods and services that satisfy people's wants and needs.

- Opportunity cost is the value of the best alternative that is given up when a choice is made (the next-best foregone option).

- Human capital refers to the knowledge, skills, education, and experience that workers acquire, which increases their ability to produce goods and services.

5.

- Land: Oil reserves, agricultural farmland

- Labor: A teacher's classroom instruction, a construction worker's physical labor

- Capital: A factory assembly line, a delivery truck

- The central government (or a centralized authority/state planners) makes all economic decisions in a command economy.

- Private individuals and businesses (driven by supply and demand in free markets) make all economic decisions in a market economy.

- A production possibilities graph is used to show the maximum combinations of two goods or services that can be produced with a fixed amount of resources and technology.

- Any point on the production possibilities curve represents an efficient level of production, where all available resources are fully and optimally used to produce a combination of goods.

- A rational decision is made when the marginal benefit of the choice is greater than or equal to the marginal cost of that choice.

- People respond to incentives by changing their behavior: they tend to pursue actions that offer rewards (positive incentives) and avoid actions that result in penalties (negative incentives).

- Specialization