QUESTION IMAGE

Question

unit 1 test study guide

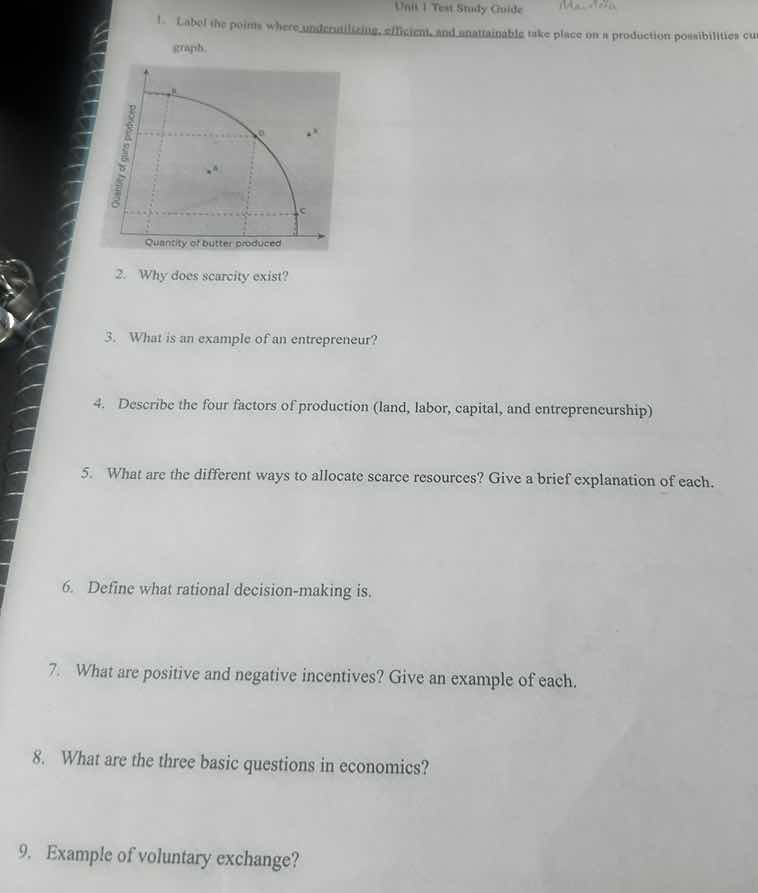

- label the points where underutilizing, efficient, and unattainable take place on a production possibilities cu graph.

(image of a production possibilities curve graph with axes: quantity of butter produced (x - axis) and quantity of guns produced (y - axis), with points a, b, c, d)

- why does scarcity exist?

- what is an example of an entrepreneur?

- describe the four factors of production (land, labor, capital, and entrepreneurship)

- what are the different ways to allocate scarce resources? give a brief explanation of each.

- define what rational decision - making is.

- what are positive and negative incentives? give an example of each.

- what are the three basic questions in economics?

- example of voluntary exchange?

Brief Explanations

- Point labels:

- Point A: Resources are not being used to full potential, so this is underutilizing.

- Points B, D, C: These lie directly on the production possibilities curve, representing maximum efficient output, so this is efficient.

- Point E: This lies outside the curve, meaning the output level cannot be achieved with current resources, so this is unattainable.

- Scarcity cause: Scarcity exists because human wants and needs are unlimited, but the resources (land, labor, capital, entrepreneurship) used to satisfy them are limited.

- Entrepreneur example: A person who starts and runs their own independent coffee shop, managing all aspects of the business from sourcing beans to hiring staff.

- Four factors of production:

- Land: Natural resources used in production, e.g., farmland, oil reserves, forests.

- Labor: Physical and mental effort of workers used to produce goods/services, e.g., factory workers, teachers.

- Capital: Man-made tools and equipment used in production, e.g., manufacturing machines, office computers.

- Entrepreneurship: The ability to organize the other three factors, take risks, and create new businesses or products, e.g., startup founders.

- Resource allocation methods:

- Market system: Resources are allocated based on supply and demand, with prices signaling value and guiding production/consumption.

- Command system: A central authority (like a government) decides how resources are distributed and what is produced.

- Traditional system: Resources are allocated based on long-standing customs, traditions, and cultural norms (common in small, rural communities).

- Lottery: Resources are assigned randomly, giving all parties an equal chance of receiving them.

- Rational decision-making: A process where individuals or entities make choices by comparing the marginal costs and marginal benefits of each option, selecting the option that maximizes their net benefit.

- Incentives:

- Positive incentives: Rewards that encourage a desired behavior, e.g., a bonus for meeting a work sales target.

- Negative incentives: Penalties that discourage an undesired behavior, e.g., a fine for speeding in a car.

- Three basic economic questions:

- What goods and services should be produced?

- How should these goods and services be produced?

- Who should receive the produced goods and services?

- Voluntary exchange example: A customer pays a bookstore $20 for a novel; both parties agree to the trade because each values what they receive more than what they give up.

Snap & solve any problem in the app

Get step-by-step solutions on Sovi AI

Photo-based solutions with guided steps

Explore more problems and detailed explanations

1.

- Underutilizing: Point A

- Efficient: Points B, D, C

- Unattainable: Point E

- Unlimited wants + limited resources cause scarcity.

- An independent coffee shop owner.

4.

- Land: Natural production resources (e.g., farmland)

- Labor: Worker effort (e.g., factory staff)

- Capital: Man-made production tools (e.g., machines)

- Entrepreneurship: Risk-taking organizer of factors (e.g., startup founders)

5.

- Market system: Supply/demand and prices guide allocation.

- Command system: Central authority (government) controls allocation.

- Traditional system: Allocation follows cultural customs.

- Lottery: Resources assigned randomly.

- Choosing options to maximize net benefit via cost-benefit comparison.

7.

- Positive incentives: Rewards for desired behavior (e.g., work sales bonus)

- Negative incentives: Penalties for undesired behavior (e.g., speeding fine)

8.

- What goods/services to produce?

- How to produce these goods/services?

- Who gets the produced goods/services?

- A customer buying a novel from a bookstore for $20.